The nonbank share of GSE servicing hit 57.8% as of the end of March, up from a 57.0% share at the end of 2023. Two of the largest banks reduced their GSE servicing during the first quarter. (Includes two data tables.)

A substantial slowdown in bulk sales of Fannie/Freddie servicing led to the lowest secondary market volume for agency MSRs since the third quarter of 2020. (Includes three data tables.)

Delinquency rates were down for all three government agencies and in every late payment category during the early months of 2024. (Includes data table.)

Production of new collateralized loan obligations as well as reset transactions in the first quarter of 2024 hit the highest level since the market reached all-time highs in 2021.

The top-line originations number held steady compared with the fourth quarter while movements in the mortgage market occurred beneath the surface. United Wholesale Mortgage regained its position as the largest lender in the first quarter.

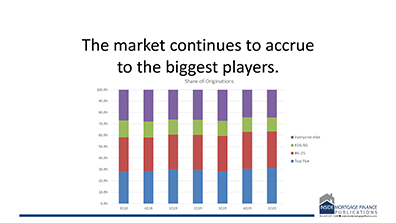

Smaller lenders, with comparatively smaller declines in volume, saw their market share rise in the first quarter at the expense of large banks and large nonbanks. (Includes two data tables.)

Servicing outstanding increased by an estimated 0.3% in the first quarter. Meanwhile, Mr. Cooper Group, which recently became the largest primary servicer, boosted its portfolio by 14.6% from the end of 2023. (Includes three data tables.)

Even though the mortgage market continued to struggle, Fannie Mae and Freddie Mac generated healthy profits in the first quarter of 2023 thanks to their business models.

All three agencies saw increases in monthly loan deliveries in April, with loan mods helping to boost Fannie to a 17.4% gain from March. The purchase market and cash-out refi remain strong. (Includes two data tables.)

Peter Norden, CEO of Homebridge Financial, is transforming his once top-40-ranked GSE lender into a HELOC originator and securitizer. Margins in conventional lending, he said, are non-existent.

Issuance of MBS backed by expanded-credit mortgages increased by nearly 50% from the fourth quarter to the first quarter of 2024. Annaly more than tripled its volume.

A recent appeals court decision against an out-of-state lender may prevent future loan modifications in California for loans with interest rates above 10%.

Agency securitizations of correspondent loans were sharply down in the first quarter of 2024 as volume dropped across the board. Refinances made a surprising surge, while credit quality remained unchanged. (Includes two data tables.)

Publicly traded banks reported a 21% increase in mortgage-banking income during the first quarter of 2024. Improving gain-on-sale margins accounted for much of the increase. (Includes data table.)

While overall correspondent sales to unaffiliated non-agency buyers declined in 2023, Veterans United increased its sales volume. (Includes data table.)

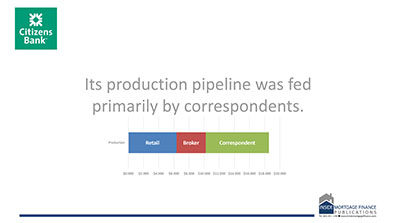

Philadelphia-based Republic Bank focused its mortgage production on jumbos with below-market rates. The bank also held agency MBS that lost value as interest rates increased.

The amount of servicing outstanding in Ginnie MBS increased by 1.6% during the first quarter. Lakeview/Bayview Loan Servicing increased its market share thanks to large purchases of MSRs.

Nonbank issuers in the Ginnie Mae program should have better access to funding from commercial banks to help bolster their liquidity, according to a proposal from the Housing Policy Council.

The Department of Housing and Urban Development’s Adrianne Todman last week made her first appearance before the Senate Banking and Housing Committee as acting secretary.

FHA and VA lenders and servicers should prepare for more regulation related to climate risk and housing sustainability, speakers at an AmeriCatalyst conference last week suggested.

Agency securitizations of correspondent loans were sharply down in the first quarter of 2024 as volume dropped across the board. Refinances made a surprising surge, while credit quality remained unchanged. (Includes two data tables.)

Servicing outstanding increased by an estimated 0.3% in the first quarter. Meanwhile, Mr. Cooper Group, which recently became the largest primary servicer, boosted its portfolio by 14.6% from the end of 2023. (Includes three data tables.)

Issuance of MBS backed by expanded-credit mortgages increased by nearly 50% from the fourth quarter to the first quarter of 2024. Annaly more than tripled its volume.

All three agencies saw increases in monthly loan deliveries in April, with loan mods helping to boost Fannie to a 17.4% gain from March. The purchase market and cash-out refi remain strong. (Includes two data tables.)

Complaints filed with the CFPB regarding mortgage servicing went up in the first quarter of 2024, while issues tied to mortgage originations declined. (Includes two data tables.)

Mortgage deliveries to the mortgage-backed securities platforms of Fannie Mae and Freddie Mac rose in April, but credit trends suggest these were seasonal increases rather than a start of a new trend. (Includes two data tables.)

The amount of servicing outstanding in Ginnie MBS increased by 1.6% during the first quarter. Lakeview/Bayview Loan Servicing increased its market share thanks to large purchases of MSRs.

Mortgage deliveries to the mortgage-backed securities platforms of Fannie Mae and Freddie Mac rose in April, but credit trends suggest these were seasonal increases rather than a start of a new trend. (Includes two data tables.)

Even though Fannie Mae and Freddie Mac maintained healthy profits in a tough market in the first quarter, their capital shortfalls under the ERCF remained absurdly high. (Includes data table.)