Embedded finance market analysis

WHAT IS EMBEDDED FINANCE — AND HOW DOES IT WORK?

Embedded finance refers to the use of financial instruments by non-financial enterprises. It allows any type of company or online store to incorporate banking software directly into their websites or mobile applications using BaaS (Banking-as-a-Service) without diverting consumers to third-party portals. Customers, for example, will no longer need to input their credit card information for each transaction and will be able to pay in installments, get insurance, and so on.

International IT consultancy Accenture looked at over 1000 non-financial businesses worldwide. In the 100 non-financial companies in the United States, it was found that 47% of respondents in the study are already investing in and planning to launch embedded finance. It turns out that 88% of those who already introduced embedded finance into their business are happy with the integration, and 85% say it helped them attract new users. Over the next five years, embedded finance growth is expected to be 215%. It will be contingent on financial service providers’ expanded availability of APIs (Application Programming Interfaces). The easy integration of these APIs will lower barriers to financial services access and give embedded financial service providers considerable new income potential.

DRIVE FACTORS

Why will the embedded payments market grow? It will be down to a number of trends, such as:

- Easy API integration for users.

- Arising proclivity to utilize financial goods from organizations that are not in the conventional banking industry, particularly for simple services like payment processing.

- Increasing desire to share personal data in exchange for more profits.

- Growth of subscription-based services. The pandemic’s trend-accelerating effects have extended to the subscription economy, which UBS predicts will rise to $1.5 trillion by 2025. That’s more than double its present value of $650 billion.

- Rapid expansion of the marketplace market (300% every year), as well as a shift in customer behavior toward e-commerce, again aided by the pandemic.

HOW WILL THE MARKETS CHANGE UNDER THE EMBEDDED PAYMENTS INFLUENCE?

There are a number of factors involved, importantly:

- Rebundling — a smooth transition from fragmented and decentralized packages of services to umbrella-like offers. Services become attractive to more categories of users, and as a result, customer base increases.

- One-stop shops — all financial and non-financial transactions are carried out in one interface (including pay-in and pay-out services).

- Open banking — to supply part of the connective tissue for the embedded financial ecosystem. Platform and product suppliers will be able to include pay-in and pay-out procedures, as well as account aggregation, providing end-to-end financial experiences. Many banks, like Halifax, Revolut, and others, have already implemented this.

MARKETPLACES BY INDUSTRIES IMPLEMENTING EMBEDDED PAYMENTS

ACTORS

Actors in the finance technology sector are identified as:

Providers. Embedded service providers produce financial services themselves that are then integrated into various platforms.

Examples: Lemonade, WealthSimple, Raisin, Affirm, and Habito.

Enablers. These are the conduits via which information and data is exchanged between providers and distributors. Data/technology infrastructure and communication capabilities are provided via APIs and Banking-as-a-Service.

Examples: Whillet, Green Dot, Railsbank, Marqeta, Plaid, and Finicity.

Distributors. This sector includes companies which pool services from many sources to create a platform or network of linked solutions that allow users to access best-of-breed solutions in a seamless manner.

Examples: Amazon, Gusto, Shopify, SmartRent, and Uber.

WHAT DO MERCHANTS GAIN FROM EMBEDDED FINANCE IMPLEMENTATION?

- High conversion rates, due to the fact that no further processes are required. Users who wish to buy anything will not be turned away due to a seamless payment system and fast checkout — there is no need for users to wait. When making a purchase, time is saved on things like loan approvals, bill settling, period for payment confirmation, and so on.

- New business methods (direct-to-customer sales, subscriptions) combined with a bid to distinguish out in a crowded market.

- Controlling cash flow (reduction of day sales outstanding).

Add to this the fact that nearly nine out of ten people (according to the Linnworks survey of ordinary shop customers) agree that having a variety of payment choices makes it easier to make decisions and encourages them to spend more. In comparison to a year earlier, 78% of shoppers now favor convenience in e-commerce.

According to a recent study conducted by Accenture, 87.5% of non-financial organizations that have begun to offer financial solutions have raised engagement levels, while 85% have drawn new clients.

TRENDS IN INDUSTRY

Health: Healthcare coverage and prices are a recurrent topic in the United States. The private health insurance industry, as well as the field of preventative medicine, offer multiple opportunities for embedded financial services. Embedded finance can fix the main problem of US private healthcare — affordability. Here it can provide the technology infrastructure that will connect healthcare providers with lenders for the flow of capital and quick and seamless financial transactions. Patients will gain improved access to healthcare services.

Real estate: There are various prospects for integrated fintech in real estate. Embedded finance allows the loan, insurance, and mortgage procedures to be integrated, making the home-buying process more fluid and individualized. Embedded financing has the potential to revolutionize the mortgage sector. One can also think of an internet platform that allows tenants and landowners to directly complete transactions, without the need of tenant brokers. Embedded financial services can help here with a variety of issues, such as deposit escrow and renter’s insurance to safeguard both sides.

Transportation: People’s modes of transportation will transform in the next few years, especially as more and more innovative transportation models emerge. Ridesharing businesses have already developed seamless payments for consumers in the transportation sector, and they are now extending this to the insurance sector by offering a special system of insurance for their cars — insurance that is only valid while they are transporting clients. This is totally different from standard continuous vehicle insurance schemes.

Municipal management: How will the city of the future look? Ideally, it should get all it can from technological progress, and from embedded finance, too. Cities have a great potential to harvest from financial digitalization. Consumers and citizens can benefit from embedded finance since it centralizes their financial data. Government institutions may find it easier to collect taxes and issue and collect fines or tickets using embedded banking systems.

PAYMENT FACILITATORS

The payment facilitator PayFac, like the payment service provider, is an intermediary, but the key difference is that PayFac independently conducts financial calculations.

Examples: Shopify, Xero, Worldpay.

The facilitator makes an agreement with the bank and receives his individual number, under which all sellers or, as they are also called, sub-merchants, are registered.

WHAT DOES PAYFAC PROVIDE?

- Fast connection, even possibly in accordance with the offer agreement.

- Single rate for connection, which includes both the bank’s commission and PayFac.

- Companies that have large ecosystems of small merchants can become payment intermediaries (PayFacs) to monetize the flow of payments between users and their customers.

Today, for example, according to Infinicept estimates, there are about 1000 PayFacs managing the processing volume of about $1 trillion. However, by 2025, we may see more than 4000 global payment systems with a processing volume of more than $4 trillion. These payment systems play a more active role in payment processing and can capture 0.75 to 1% of the transaction volume in exchange for taking on the risks and operations associated with the collection of payments. Traditional PayFac solutions allow platforms to embed card payments into their software and monetize payments faster, as well as whitelist other financial services, such as issuing cards and loans.

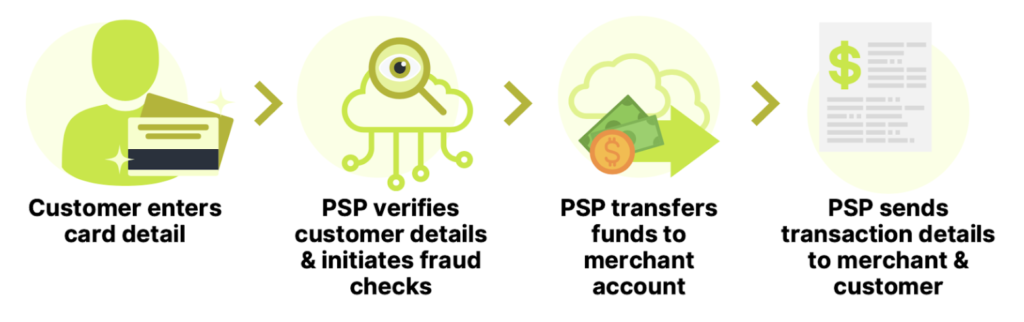

PSP

Payment service providers (PSPs) are third-party firms that assist businesses in implementing a variety of online payment methods, including credit cards, debit cards, e-wallets, and online banking. Transaction protection is ensured by PSPs. They are an integral aspect of the payment ecosystem, which links sellers, consumers, financial institutions, and payment networks. Gateway capability is provided by PSPs to merchants and their customers.

Organizations that outsource processing do not have control over their trade contracts. They rely on an external system when adopting an outsourced payment model, which becomes an important component of their consumers’ experience. If sellers want to transfer to a competitor platform, the lack of ownership rights could be a concern.

HOW DOES PSP WORK?

CONCLUSION

To sum up, embedded finance, rather than reselling financial services, is appealing to digital brands and sellers because it generates new revenue streams at very low marginal costs. Brands that implement it usually already have customer bases and embedded finance helps them to develop a more qualitative approach to revenue generation by creating a unique client experience that encourages loyalty and repeated purchases, as well as allows merchants to better understand the trends behind customers’ attitudes and approaches to shopping.

As regards white label payments from payment service providers it can be difficult to monetize via extra charges markups without shifting additional costs to the buyer. Consumers’ expectations for adaptable financing, the emergence of plug-and-play technology solutions that permit enterprises to lend to clients (i.e., lowered entry barriers), and the range of available (alternative, non-financial) data sources that allow businesses to effectively underwrite their consumers are all factors that have contributed to the rising trend of embedded finance.